ARTICLES

Market Insight- May 2026

Why We're Not Panicking About Australia's Rate Hikes & Tax Reform Headlines

The media storm around Australia's interest rate hike and negative gearing reforms is loud. Here's what the data actually says — and why long-term property investors have every reason to stay the course.

By Myfingraph Research Team ♦️ May 2026 ♦️ 10 mins ReadMM

| 1.0% | 3.5% | 2.2% | $0 |

|---|---|---|---|

| National vacancy rate (Mar 2026) | Projected annual rent growth (KPMG) | DP growth forecast 2027 (IMF) | New tax legislation actually passed (yet) |

Every time rates move or a politician mentions negative gearing, the headlines scream crisis. We prefer to read the actual RBA report, study the vacancy data, and let the numbers do the talking. Here is our calm, data-driven read of where Australia stands right now — and where it is headed.

Setting the scene

Yes, Rates Went Up. Here's the Full Picture.

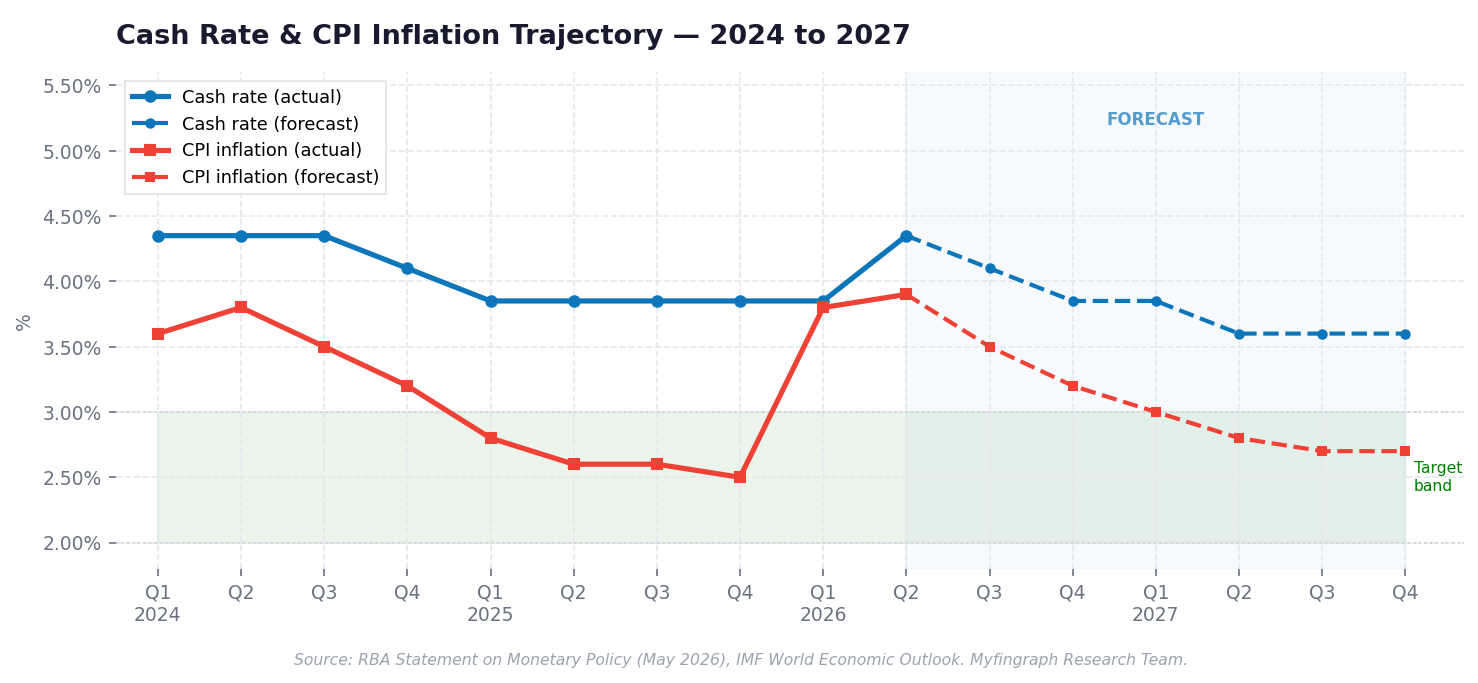

The Reserve Bank of Australia raised the cash rate by 25 basis points to 4.35% at its May 2026 board meeting. Cue the panic. But before you do anything drastic with your portfolio, let's zoom out.

The RBA's own Statement on Monetary Policy confirms what caused this: a global fuel price surge driven by Middle East conflict — an external shock, not a structural collapse of the Australian economy. The board was clear: spending is already slowing, the jobs market remains healthy, and the economy is expected to find its footing through 2026 into 2027.

"The economy is likely to slow this year — but the jobs market is expected to remain healthy, and inflation is forecast to return toward the target range."

— RBA Statement on Monetary Policy, May 2026

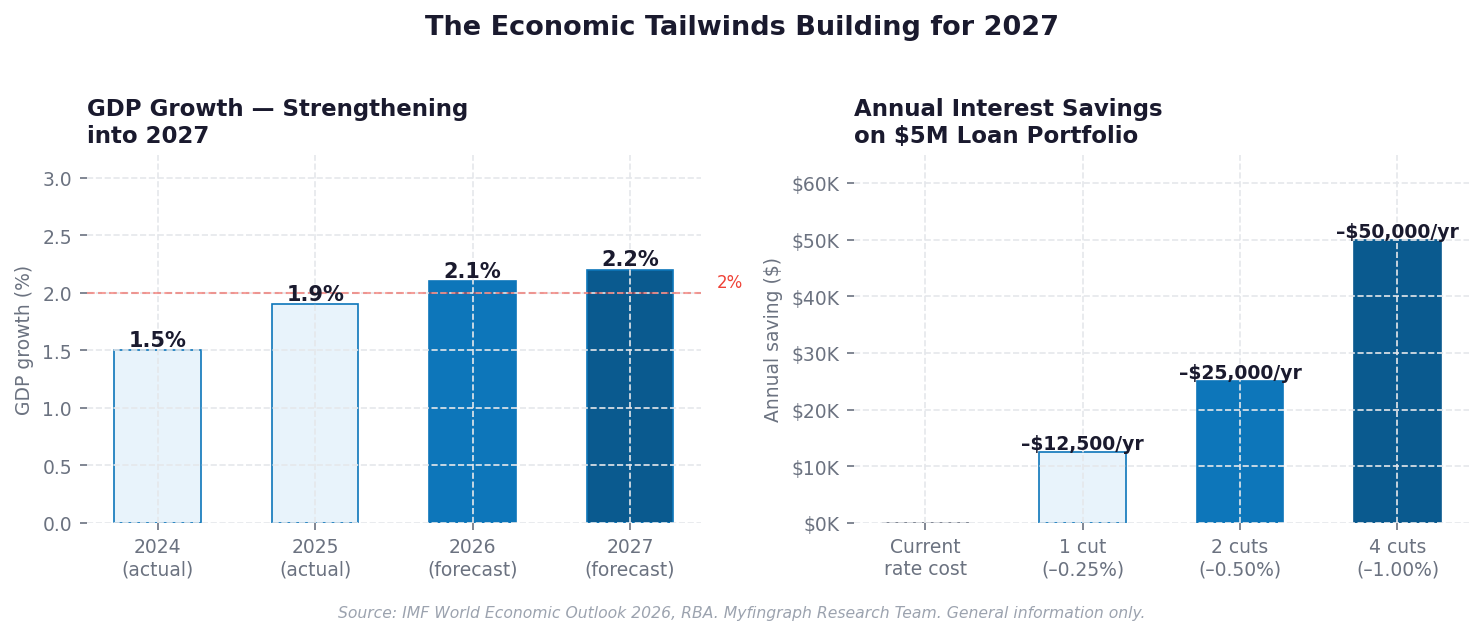

This is a late-cycle rate adjustment in response to a temporary global shock — not the beginning of a decade of tightening. The IMF projects Australian GDP growth will actually accelerate to 2.1% in 2026 and 2.2% in 2027 as prior monetary easing flows through the economy. That is not a recession story. That is a soft landing.

Chart 1: Cash Rate & CPI Inflation Trajectory — 2024 to 2027. Source: RBA, IMF, Myfingraph analysis.

The Myfingraph Take

Rate cuts are on the horizon — not in the distant future. Our base case sees the RBA begin easing by late 2026 or early 2027 as inflation tracks toward the 2–3% band. Every 0.50% of cuts translates to roughly

$25,000 in annual savings on a $5M investment loan portfolio. Patience is a strategy.

The rental market

The Rental Market Is Sending a Very Different Signal

While rate conversations dominate the headlines, the rental market is quietly telling a powerful story for property investors — one that the media largely ignores.

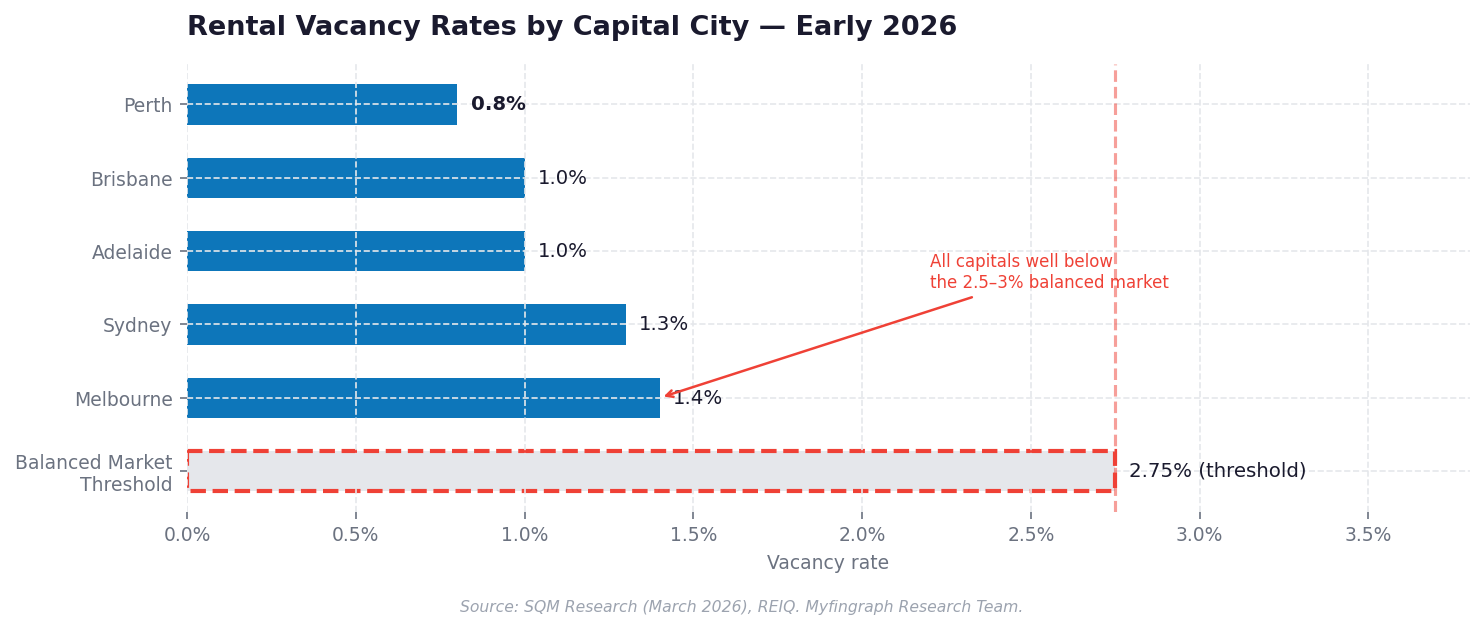

Australia's national residential vacancy rate hit 1.0% in March 2026, down from 1.1% in February. For context, a "balanced" rental market sits between 2.5% and 3%. We are at less than half that. In practical terms, this is one of the tightest landlord markets in Australian history.

Chart 2: Rental Vacancy Rates by Capital City — Early 2026. Source: SQM Research, REIQ, Myfingraph analysis.

What is driving this? Three structural forces that are not going away anytime soon:

• Population surge: Migration is driving housing demand significantly faster than new supply can be delivered. Queensland alone accounted for 25% of national population growth since 2020 but less than 20% of dwelling completions.

• Construction gridlock: Building costs, labour shortages and planning delays mean the pipeline of new rentals remains well below what is needed. KPMG estimates completions would need to be 17% higher than current forecasts just to normalise rental growth.

• Buyers locked out: Higher rates have kept many would-be buyers in the rental pool longer, adding sustained demand pressure that shows no sign of reversing until meaningful rate cuts arrive.

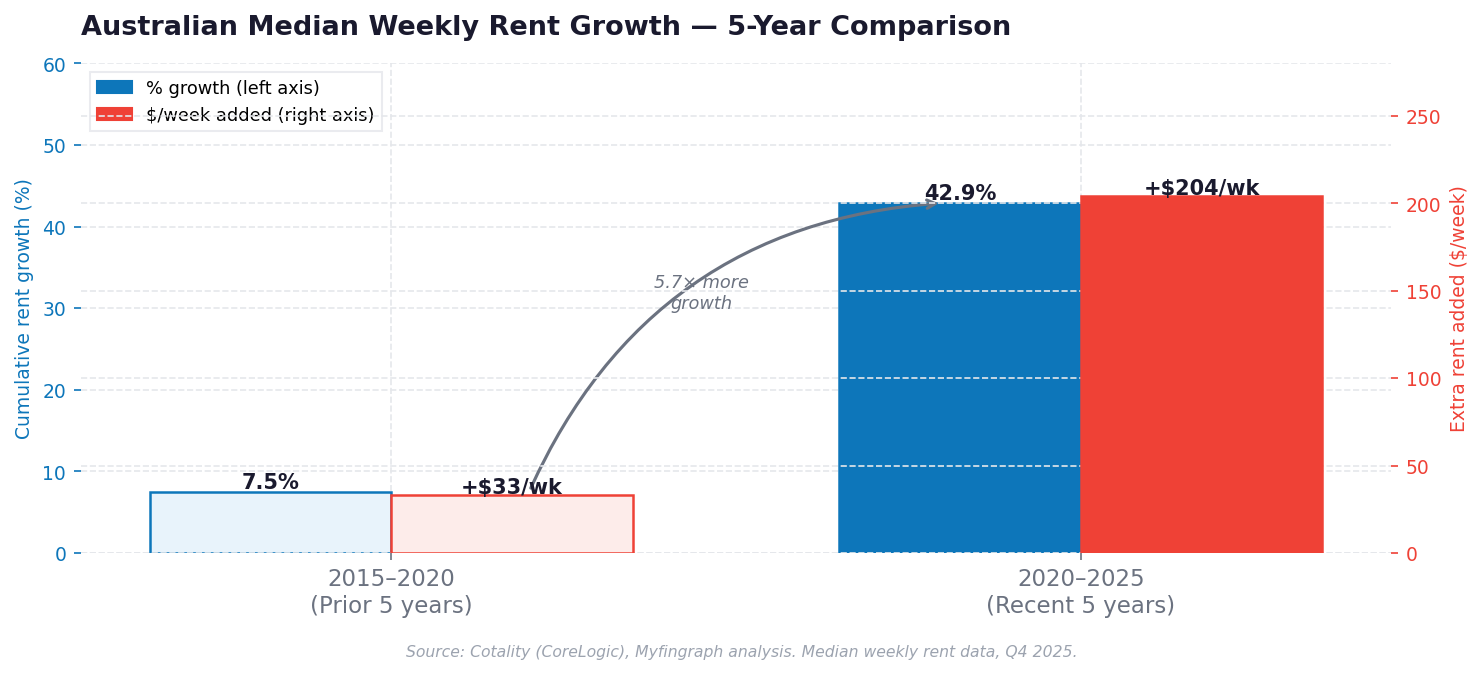

Chart 3: Australian Median Weekly Rent Growth — 5-Year Comparison. Source: Cotality (CoreLogic), Myfingraph analysis.

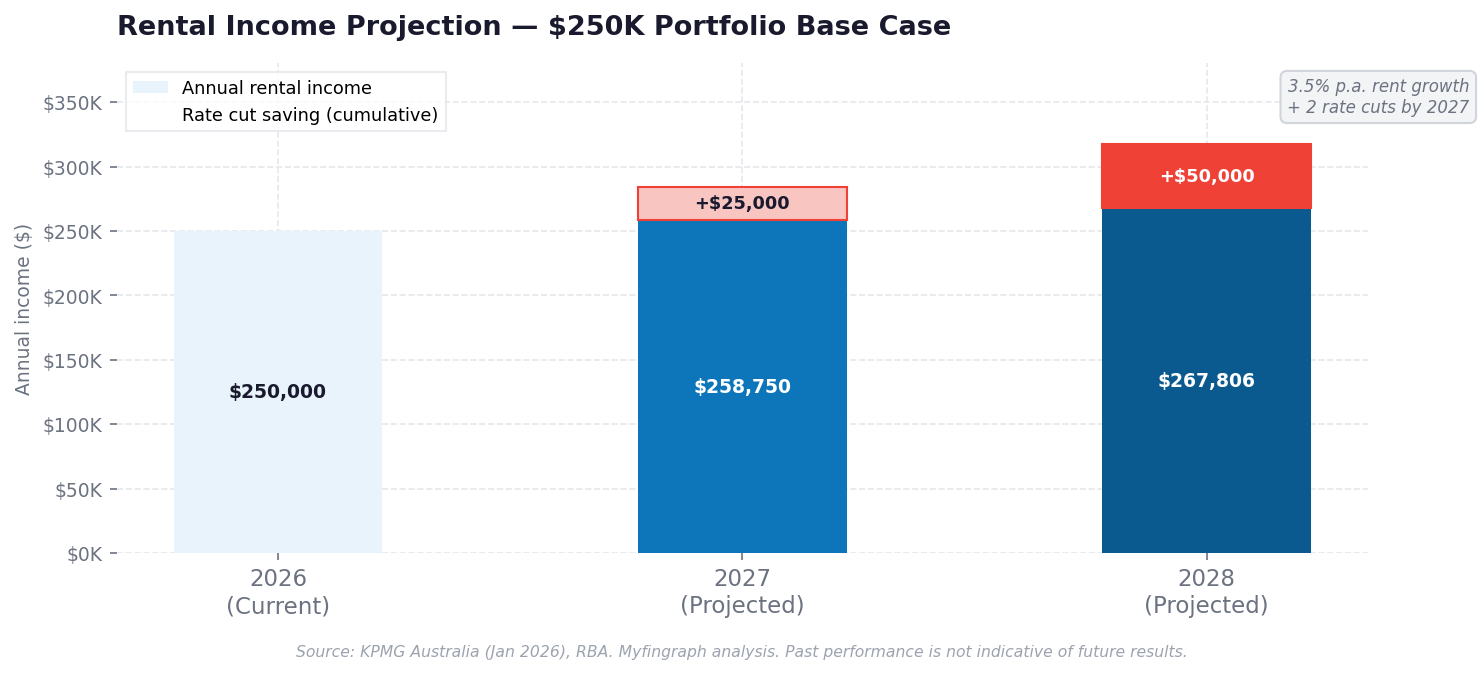

KPMG's January 2026 outlook projects

3.5% annual rent growth through 2026 and 2027. For a portfolio generating $250,000 in annual rental income today, that is an additional ~$17,500 in income by year two — with no extra properties, no extra effort.

IRONICALLY

If negative gearing reform does pass in its harder form and deters new investors from entering the market, rental supply tightens further — which supports even stronger rent growth. The reform the media says will hurt investors may actually strengthen their income position in the short-to-medium term.

Tax reform reality check

Negative Gearing & CGT Reform: What's Real, What's Noise

This is the topic generating the most anxiety among our clients. So let's be precise about what we actually know as at May 2026.

Important — Current Status

No negative gearing or CGT legislation has been passed. As at May 2026, these remain proposals under active government consideration — not law. The May federal budget is the decision point. Do not restructure your portfolio based on what might happen.

That said, being prepared is not the same as panicking. Here is what the most credible reform models on the table actually look like — and crucially, what they almost certainly will not touch:

| Reform Proposal | What Changes | What Is Protected | Risk Level |

|---|---|---|---|

| Negative gearing cap | Deductions limited to first 2 investment properties | Existing holdings likely grandfathered | Medium |

| CGT discount cut | 50% reduced to 33% on assets held 12+ months | Pre-cutoff acquisitions grandfathered | Medium |

| Loss quarantining | Losses offset only against property income | May exclude new builds to protect supply | Higher |

| CGT 6-year rule | No change proposed | Former PPOR exempt for up to 6 years | Low |

| Family home CGT | No change proposed | Primary residence remains fully exempt | Low |

The political reality also matters here. The government needs the Greens to pass any reform through the Senate, and the Greens want stronger reform than what Labor is proposing. The Coalition has signalled it will not support cuts. The result will almost certainly be a softer compromise than the headlines suggest — one that heavily protects existing investors through grandfathering.

"Grandfathering has featured prominently in the discussion, with pre-reform assets likely to keep their current tax treatment. That was part of Labor's earlier approach and would limit the effect on investors who bought before any new rules took effect."

— Australian financial commentators, April 2026

What smart investors do now

The 5 Things Calm Investors Are Doing Right Now

Being unshaken by headlines does not mean being inactive. Here is what considered, long-term investors are focusing on in this environment:

1. Document everything

Record the acquisition date of every property now. Grandfathering will almost certainly be date-based. This is the single most important preparation step you can take before budget night.

2. Model your CGT position

Run two scenarios with your accountant: 50% vs 33% CGT discount on each asset. Know your after-tax proceeds before making any sell decision. Selling without modelling first is how investors leave money on the table.

3. Review your 6-year rule

If any property was previously your primary residence, check whether you are within the 6-year CGT exemption window. This rule is not currently targeted by reform — and it is one of the most underused strategies in property investment.

4. Focus on yield quality

In an environment where negative gearing may become more restricted, properties with strong rental yields hold up better. A well-tenanted, cash-flow positive property in Brisbane or regional QLD is more resilient than a low-yield speculative asset.

5. Don't rush, but don't freeze

If you were already planning a purchase with strong fundamentals, there is a reasonable case for prioritising the next 60–90 days under current rules. But buying a poor property in a panic to beat a budget announcement is not strategy — it is anxiety dressed up as action.

Chart 4: Rental Income Projection — $250K Portfolio Base Case. Source: KPMG, RBA, Myfingraph analysis.

The long view

Why We Remain Confident in Australian Property for 2027 and Beyond

Let's end where every good investment analysis should — with fundamentals, not feelings.

Australia has a structural housing shortage that neither a rate hike nor a budget announcement can fix overnight. Population is growing. Construction is lagging. Renters are paying a record 33.4% of their pre-tax income in rent because they have no other option. That dynamic does not reverse when a headline changes.

Brisbane is recording house price growth of up to 17% annually. Regional Queensland markets are outpacing capital cities on both price and yield. Perth and Adelaide remain critically undersupplied. The Melbourne Metro Tunnel is already generating price premiums in corridor suburbs. These are durable tailwinds — not noise.

Chart 5: GDP Growth Trajectory & Interest Rate Savings Outlook — 2024 to 2027. Source: IMF, RBA, Myfingraph analysis.

| GDP 2027 | Rents | Rate cuts ahead |

|---|---|---|

| IMF projects 2.2% growth — stronger than 2026. The economic soft landing is taking hold | 3.5% p.a. forecast income growth. At 1% vacancy, landlords retain strong pricing power through 2027 | Our base case sees 2 cuts by end 2027, saving ~$25,000 p.a. on a $5M loan. The cycle is turning. |

"The same factors that have supported value growth — restricted advertised supply, strong rental demand, and population inflows — will likely continue to support growth in 2026 and beyond."

— Cotality (CoreLogic) Research, 2026

Our message to every client who has called us concerned about the headlines this week is the same: the noise is loud, but the fundamentals are sound. We have been through rate cycles before. We have seen tax reform debates before. Long-term Australian property investors who stayed calm, stayed invested, and stayed strategic have consistently come out ahead.

That is exactly what we intend to keep doing — and we would love to help you do the same.

Want a Personalised Portfolio Review?

We are helping investors model the impact of every scenario — rate cuts, tax reform, rental income growth — specific to their portfolio.

www.myfingraph.com.au/book-now

Disclaimer: This article is general information only and does not constitute financial, legal or tax advice. All forecasts are based on publicly available sources including the RBA Statement on Monetary Policy (May 2026), IMF World Economic Outlook, KPMG Australia, SQM Research and Cotality (CoreLogic). Tax reform proposals referenced are not yet enacted legislation — outcomes may differ materially from those discussed. Readers should consult a licensed financial adviser and registered tax agent before making investment decisions. © 2026 Myfingraph. All rights reserved.

Recent News