ARTICLES

BUDGET TAX REFORM SERIES

The Budget Changed the Rules. Your Investment Strategy Didn't Have To

Understanding the Negative Gearing Changes — May 2026 Budget

We never built your portfolio around a tax refund. That’s why this doesn’t change much for us at all.

By Myfingraph Research Team ♦️ May 2026 ♦️ 10 mins ReadMM

Let’s Start With What Everyone Is Getting Wrong

If you’ve been scrolling through the news this week, you’ve probably seen headlines screaming that negative gearing has been “scrapped” or “killed off.”

Take a breath.

It hasn’t.

What changed on 12 May 2026 is not the end of negative gearing. It’s a change in the timing of the tax benefit — and for long-term investors like you, the impact is smaller than you think.

Here’s the simple version:

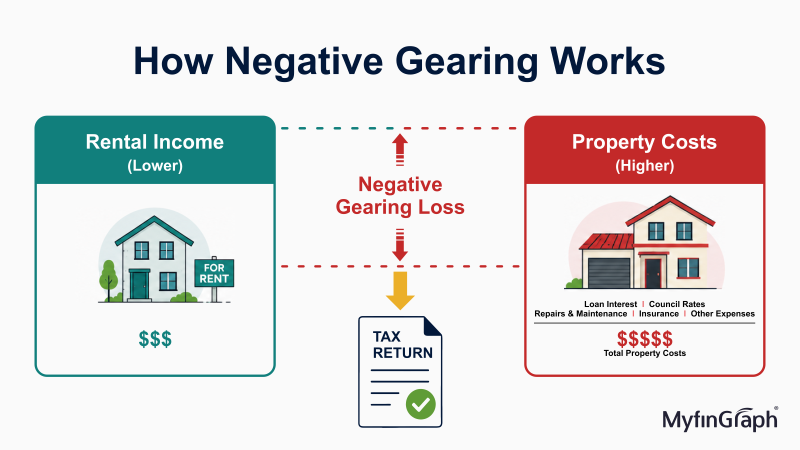

Before Tuesday, if your investment property was running at a loss, you could reduce your tax bill right now — in the same financial year — and often get a refund.

From 12 May 2026, for new purchases of existing residential properties, those losses still exist — but instead of getting the tax back immediately against your wages, the losses are saved up and used later, when your property starts making a profit.

That’s it. That’s the main change.

The loss didn’t disappear. It just got a “see you later” stamp on it.

Here’s a Simple Way to Think About It

Imagine you lend a friend $10,000 to start a business. In year one, the business makes a loss.

Under the old rules, you could write off that loss today and get a chunk back from the taxman right away.

Under the new rules, you still record that loss — but you use it later, when the business starts making money, to reduce the tax you pay on the profits.

Either way, the loss counts. It’s just a matter of when it helps you. For a long-term property investor, this is a timing difference — not a loss of benefit.

What Myfingraph Has Always Believed

Here’s the honest truth about how we’ve always approached this.

We never built your investment strategy around negative gearing as the main event. We never said, “Buy this property because you’ll get a great tax refund every year.”

What we said — and still say — is this:

Buy the right property, in the right location, hold it long enough, and let the market do the heavy lifting

Negative gearing, when it existed in its old form, was simply a nice advantage in the early years — a bit of help while the property grew into its own. A bonus on the journey. Not the destination.

That hasn’t changed. What changes is when the bonus arrives.

What This Means for You — Right Now

If you bought your property before 12 May 2026:

Nothing changes. Not a single thing. The old rules apply to everything you already own. Your negative gearing, your tax treatment — fully intact. This is called grandfathering and the government has confirmed it clearly.

If you’re wondering about your SMSF properties:

Good news. The changes do not apply to SMSF investment properties. Our work on the SMSF side continues exactly as before. If you’ve been planning to grow your super through property, that pathway is still fully open.

If you’re thinking about buying something new:

This is where we adapt — and we already are. More on this in Article 3.

The Numbers Still Work — They Just Look a Little Different

Let’s keep it simple with an example.

Say you buy an investment property after 12 May 2026 and it runs at a $10,000 loss in year one.

Previously, that $10,000 loss might have reduced your tax bill immediately — depending on your income bracket, you may have received $3,000 to $4,000 back at tax time.

Now, that $10,000 loss is recorded and carried forward.

Fast forward a few years. Your rent has grown. Your loan balance has dropped. The property tips into profit.

That’s when those stored-up losses start doing their job — reducing the tax you pay on your property profits.

For a buy-and-hold investor, this aligns beautifully with the natural arc of property ownership. Early years: the property builds and grows. Later years: it produces income. That’s exactly when those deferred losses become useful.

Why Long-Term Strategy Always Wins

Here’s something worth sitting with.

The wealth in property has never come from the annual tax refund. It has come from capital growth — the property being worth significantly more in 10, 15, 20 years than what you paid for it.

Someone who bought in the right suburb a decade ago and held on is not sitting there counting their yearly tax refunds. They’re sitting on an asset that has potentially doubled in value.

That’s the game. That’s always been the game.

This budget change does one thing well: it separates the long-term thinkers from the people who were investing primarily for a tax outcome. For the first group — the ones we work with — the strategy remains sound.

What Has NOT Changed

Let’s be really clear on a few things:

- Your weekly and monthly cash flow is exactly the same. The property still costs what it costs to hold.

- All properties purchased before 12 May 2026 are fully protected under the old rules.

- SMSF property investment is not impacted by these changes.

- Commercial property is not impacted. Only residential properties are affected.

- The losses on new purchases don’t disappear — they are carried forward and used when the property produces income.

- Governments change. These rules could be reversed or amended in future years. You don’t want to be sitting on the sidelines, only to watch the market move without you.

Coming Up in This Series

This is Article 1 of 3.

Article 2 will cover the Capital Gains Tax changes — also announced in this budget — and what they mean for when and how you might sell.

Article 3 will walk through the strategies we are actively building for new purchases in this new environment. There are smart ways to approach this, and we’re already working on them with clients.

Final Thought

We’ve always said that property investing is a long game. Tuesday’s budget just made that more obvious.

If you’re sitting on a well-selected property and holding it with a clear long-term view, this change is far more of a ripple than a wave.

Please reach out. That’s exactly what we’re here for

If you have questions about what this means for your specific situation — your existing properties, your SMSF, or what you’re planning to buy next: www.myfingraph.com.au/book-now

Disclaimer: This article is not financial advice. The circumstances of individuals may differ, and you must get financial advice where necessary. What follows here is our personal and subjective opinion. It's based on simple strategies that have helped us and our clients earn great income over the years.

Recent News